Once you register a company, it may seem like everything is set in stone.

The requirements have been completed, the paperwork filed, and the business is up and running.

Even in the midst of operations, however, there are ways to adjust your company as it continues to grow.

A business entity can change its name, a sole proprietorship can restructure as a partnership, and a corporation can relocate its headquarters.

One available option for a limited liability company (LLC) is to change the way it’s taxed.

Certain classifications can work better for certain companies, potentially saving a good deal in taxes each year.

Depending on the classification, the change can be made by filing either Form 8832 or Form 2553 with the Internal Revenue Service (IRS).

This article goes over the basics of both IRS forms, the advantages and disadvantages of each, and what they mean to a company.

- An LLC’s Default Tax Classification

- What Is Form 8832

- How to File Form 8832

- Advantages of C Corp Classification

- Disadvantages of C Corp Classification

- What Is Form 2553

- How to File Form 2553

- Advantages of S Corp Classification

- Disadvantages of S Corp Classification

- Deciding to Change Your LLC’s Tax Classification

An LLC’s Default Tax Classification

When an LLC is formed, it is automatically assigned a default tax status or classification based on how many business owners or “members” it has.

A single-member LLC is considered a “disregarded entity” by the IRS, meaning that the company is ignored and the owner is simply taxed as a sole proprietor.

A multiple-member LLC with two or more owners is taxed as a partnership.

Both structures are considered “pass-through,” meaning all company taxes are passed through to the personal tax returns of each member.

An LLC isn’t required to file a company tax return, although multi-member LLCs do have to file a 1065 partnership return and a K-1 for each of their members.

This default tax classification, however, may not be the best one for you.

A company can possibly save thousands of dollars in annual taxes just by changing how it’s taxed.

And since an LLC has the option to elect for a preferred tax classification, its owners should pick the one that provides the biggest benefits and savings.

The most common classifications selected by an LLC are either C Corporations (C Corps), which require Form 8832, and S Corporations (S Corps), which require Form 2553.

Each classification offers its own advantages and disadvantages, depending on the company.

Speak with an accountant or financial advisor to decide on the best tax classification for your LLC.

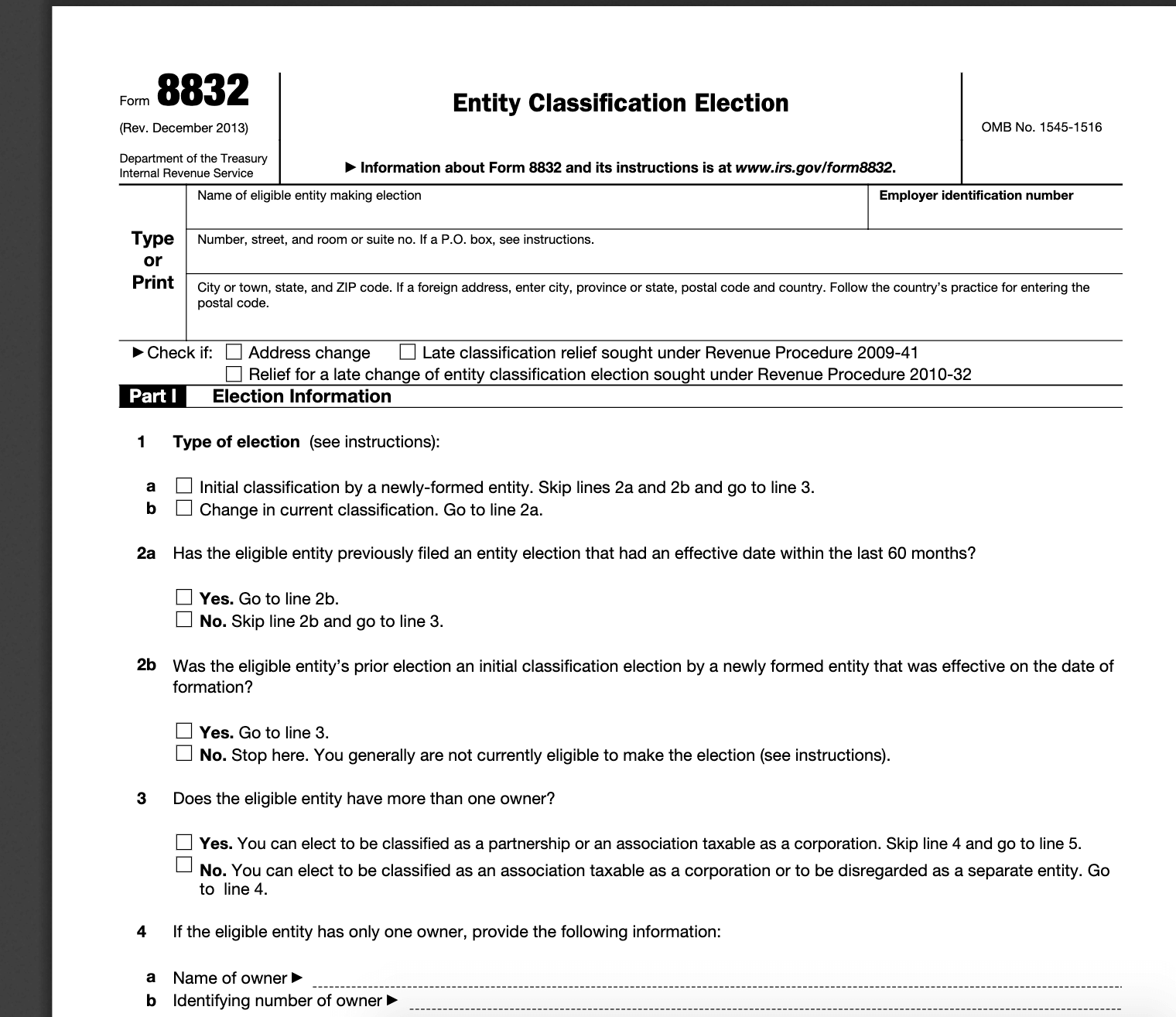

What Is Form 8832

Form 8832 is an eight page document, five pages of which are instructions.

It’s also referred to as an “Entity Classification Election” and is filed with the IRS.

Only a few eligible entities are allowed to file Form 8832.

These include partnerships, LLCs, and some foreign entities.

Those not allowed to file include insurance companies, businesses owned by a state or foreign government, state-chartered banks (if FDIC-insured), tax-exempt organizations, and real estate investment trusts (REITs).

A company files Form 8832 if they want to elect for a new tax classification, either as a sole proprietorship, partnership, or C Corp.

Before filing Form 8832, owners are obligated to first file articles of incorporation with their secretary of state.

Each state has different incorporation requirements so it’s best to do research for the state in which the organization wishes to incorporate.

How to File Form 8832

You can download Form 8832 from the IRS website, along with a set of instructions for how to complete it correctly.

The form begins with a series of questions regarding the entity’s basic information and current classification and ends with the official consent of all the members.

This requires listing their complete names, social security numbers, and signatures, as well as the company’s employer identification number (EIN).

File the completed Form 8832 with the IRS Service Center for your state and include a copy of the form when filing your next business tax return.

While there is no deadline for filing — it can be when you register the business or any point thereafter — the time you file does have an effect.

If approved, the new classification can only have an effective date up to 75 days before filing the form or for up to one year after filing the form.

If the desired date has already passed, the form also includes a section where the LLC can apply for late election relief.

This is usually granted only with reasonable cause, which must be sufficiently proven when submitting the form.

The IRS will usually send their decision of acceptance or non-acceptance within 60 days of filing.

Advantages of C Corp Classification

Although not a common choice among small businesses, being taxed as a C Corp does offer advantages in certain situations.

It’s particularly beneficial for those looking to raise money or go public, as it creates a more formal corporation.

It also opens the company to an unlimited number of shareholders and generally makes the transfer of shares much easier.

On the tax side, being classified as a C Corp allows a business to use the fiscal year, which spans two calendar years and offers greater leeway to manage the company’s cash flow.

If the owners are also employees, they may be entitled to a number of fringe benefits.

A notable one being the self-insured medical reimbursement plan under Section 105(b), which allows the company to pay all medical expenses not reimbursed by insurance.

C Corps can also avail of the widest range of tax deductions, including operating expenses, marketing expenses, travel expenses, legal fees, medical and retirement plans for employees, and the like.

Done properly, this can ultimately lead to reduced tax rates.

There are a variety of benefits an LLC may gain from this tax classification.

However, knowing how to reap them is not a task for the inexperienced.

Work with a financial or tax professional to make sure you’re putting your company in the best financial position possible.

Disadvantages of C Corp Classification

Although taxes vary per business, C Corps tend to pay the highest taxes.

This goes for taxes across the board, from annual tax returns to capital gains tax (paid whenever an asset is sold).

A C Corp classification is not only subject to federal income tax, but state and local taxes, as well (although some states may allow you to deduct a percentage of federal taxes).

C Corp owners also get hit with “double taxation” — once on the corporate level (about 21%), and again at the personal level (when they receive any salary or dividends, about 10-37%, depending on the income level).

So from being part of a standard LLC that doesn’t require a separate tax return, members of an LLC with a C Corp tax classification must now file business tax returns, in addition to their individual income tax returns.

The owner of an LLC with a C Corp tax classification can also no longer write off business expenses on their individual tax returns.

This can only be done on the business tax returns.

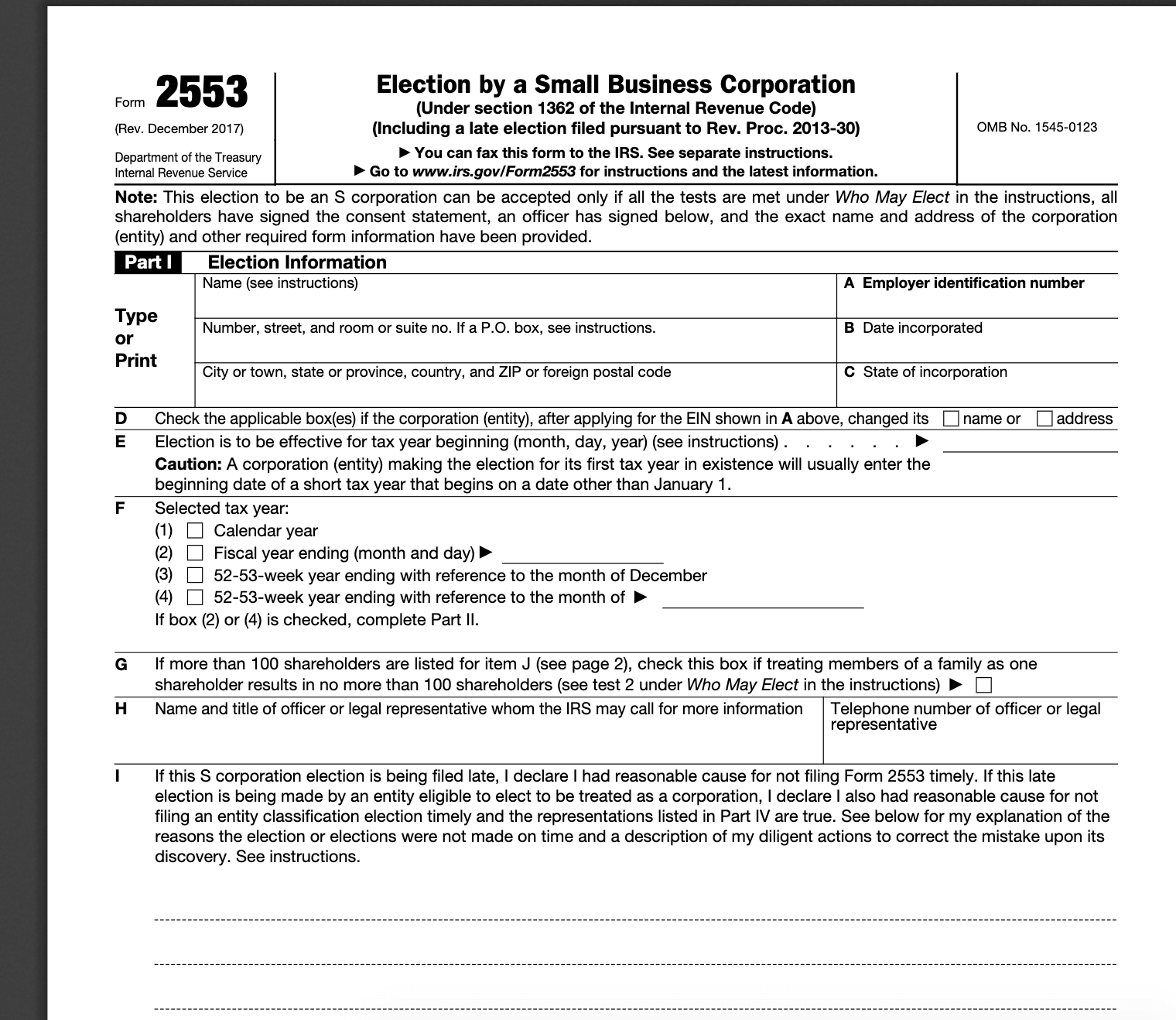

What Is Form 2553

Form 2553, also called “Election by a Small Business Corporation,” consists of four pages, accompanied by another six pages of instructions.

By filing the form with the IRS, an LLC or C Corp is electing to be taxed as an S Corp, usually in order to lower taxes.

S Corps are corporate entities that are very similar to C Corps with the main difference being their tax classification.

S Corps are pass-through entities that don’t pay business tax.

Rather, all earnings are declared using the owner’s personal income tax return.

To file Form 2553, an entity must be a domestic corporation with only one class of owners (no preferred shareholders or members).

It must also have no more than 100 shareholders who must all be citizens or residents of the United States.

If an S Corp grows to over 100 shareholders, it loses this classification and is treated as a C Corp.

An exception to this is if two or more shareholders are from a single family, they may opt to be counted as a single shareholder.

The following entities are ineligible to apply for S Corp classification: insurance companies, bank or thrift institution that uses the reserve method of accounting for bad debts, possessions corporations, and domestic international sales corporations (DISCs).

How to File Form 2553

Form 2553 can be downloaded from the IRS website, along with a corresponding set of instructions.

The form is divided into four parts.

The first is the only required part, collecting all basic information: the company’s name, address, EIN, incorporation details, and the consent of all shareholders.

The remaining three parts may be skipped, unless the company is requesting a non-calendar tax year based on a specific business purpose, one of the shareholders is a Qualified Subchapter S Trust (QSST), or the company is filing after the tax deadline.

Form 2553 must be filed no later than two months and 15 days after the beginning of the tax year the election is to take effect, or any time during the preceding tax year.

The form can be filed through mail or fax — it can’t be filed online.

If mailing, send only the original form (no photocopies), and if faxing, make sure to keep the original together with the company’s other files.

The exact address or fax number for your location can be found on the IRS website.

After submission, you can expect to hear a response from the IRS within 60 days (add an additional 90 days if you opted for a non-calendar tax year based on a specific business purpose.)

Accepted tax classification changes stay in effect until the company dissolves or elects to change its tax classification again.

If S Corp status is terminated or revoked, a company usually can’t re-apply for S Corp tax classification until a span of five years has passed.

There is generally no fee to submit Form 2553, but companies opting for a non-calendar tax year are charged a $5,800 fee.

Late submissions may also incur additional charges.

Do not send any payments with the form.

Rather, the IRS will send a separate bill with payment instructions.

Advantages of S Corp Classification

While both LLCs and S Corps are pass-through entities and aren’t required to file business tax returns, a good reason to prefer S Corp tax classification is for employment tax.

In S Corps, an owner (who also works as an employee in the company) doesn’t have to pay self-employment tax for all of the company’s income — only for their salary.

This is because in an LLC, the owner is considered an owner.

In an S Corp, on the other hand, the owner is considered an employee.

So they pay tax on their salary.

But not on all their other income from the business (dividends, etc.).

Note that as with any employee, salaries are also subject to Social Security and Medicare taxes, paid half by the employee and half by the corporation.

With the correct structure and tax treatment, this income-splitting can potentially save owners a good chunk in taxes.

The recently-implemented Tax Cuts and Jobs Act (TCJA) may also be very beneficial, as it gives pass-through entities a 20% qualified business income deduction.

As always, we advise that you seek financial advice from a professional about the best, most beneficial way to structure your business.

Disadvantages of S Corp Classification

Being taxed as an S Corp may be disadvantageous for certain businesses and owners.

For example, shareholders with two or more percent shares can no longer receive tax-free benefits.

Company shares are also now subject to seizure and sale in court proceedings.

An S Corp is not suitable for companies that wish to hold appreciating investments because capital gains for the sale of assets will incur higher taxes, nor is an S Corp good as an estate planning vehicle because control is ultimately in the hands of the shareholders.

S Corps are also limited to having only one class of share.

Deciding to Change Your LLC’s Tax Classification

Keep in mind that changing an LLC’s tax classification, whether to a C Corp or an S Corp, is solely for tax purposes.

An LLC will still function as is in every other way, and its legal status remains the same.

That being said, changing a company’s tax classification is a complex issue and may have other effects you should be aware of.

Take the time to discuss it thoroughly with a financial or tax professional to find out which classification is best for your LLC.